- ፍራንክ Digest

- Posts

- Cheques & Balances

Welcome to the latest edition of ፍራንክ Digest!

Your weekly brief on all things Finance and Investing. Quick, enjoyable reads for busy professionals in 5 minutes or less.

What we’ve got in store for you:

🔏 Cheque Please: The Fine Line Between Promise and Peril

🔪 Slice It Up: The 50/30/20 Savings Rule Made Easy

🗝️ The Key Takeaways

Thanks for reading!

Are Cheques Still a Safe Bet?

Banking

Is it cheques or checks? Depends on whether you want to sound broke in British or American—cause they bounce the same!

In the ever-evolving world of finance, the humble cheque has long been a staple of personal and business dealings, faithfully representing a promise to pay long before digital payments took the stage.

It’s like the classic watch in a world of smartwatches—timeless and dependable, even if a little old-fashioned. However, the question of whether cheques can still be used as payment guarantees has been a topic of ongoing debate and legal scrutiny in Ethiopia.

Originally, these pieces of paper were the go-to for moving money around—back in the days before mobile apps made life easy and let people and businesses transfer funds in a breeze.

Fun fact: cheques go way back, like 3rd century B.C. back, when the Indian Mauryan empire used them as fancy IOUs.

Fast forward, and our humble paper has transformed into a versatile financial tool, evolving from a basic promise to pay into something much more complex.

One of the primary concerns is the risk of fraud, which brings to mind the movie Catch Me If You Can (based on true events ባይ ዘ ወይ!). Whether it is a counterfeit or over-drawing accounts, this has led to a growing awareness of the need for banks to employ robust security measures and careful scrutiny of transactions (ፈራሚ ኖት?…ይከፈል?).

In Ethiopia, writing a bad cheque—whether it’s fake or funds are low—can land you in hot water with serious consequences according to the country's civil and criminal laws: blocked accounts, penalty fees, National Bank of Ethiopia (NBE)’s naughty list and in the worst cases a one-way ticket to jail!

If you choose to lawyer up & litigate, you must have the cheque in hand and any fine print detailing the conditions of your transaction. Depending on how much we're talking—less or more than ETB 500k—you might need to show up at either the First Instance Court or the Federal High Court.

Rest assured, the process is slower than a snail on vacation regardless!

A more appropriate payment guarantee would be a Cashier’s Payment Order (CPO). A CPO either locks the amount in the Payer’s account or loans it to the Payer with interest, all for a small fee.

This service is offered both by banks and insurance companies. It would put the Payee more at ease of receiving their money when due and encourage more trade opportunities.

As our economy develops and legal frameworks continue to evolve, the role of the cheque in financial transactions is likely to undergo further scrutiny and refinement.

In short, while cheques are still around, they’re not always the best bet for payment guarantees. Using a CPO might just be our ticket to smoother, more secure transactions.

ፍራንክ Picks

🚶🏽 Event [Sep 19-20, Sheraton]: East Africa International Arbitration Conference 2024

🗞️ In the news: Changing seats → Amhara Bank recruits former DBE head

♟️ Innovation of the week: Lomii throwing goes digital

🔔 Check out our Telegram t.me/frankdigest where we post snippets and interesting quizzes!

Budget Like a Boss: The 50/30/20 Universal Savings Rule?

Personal Finance

✋🏽 Raise your hand if you’ve ever set yourself a budget for a month and actually stuck to it?

If you’ve raised your hypothetical hand, then you’re in the minority and congrats to you!

Sticking to a plan, especially when it comes to money, can be daunting.

Think about it, budgeting or saving (to put a more positive spin on it) is not fun: it limits your decision making, usually foregoing short term satisfaction for long term reward!

On top of that የሚያሳስት ወገን ደግሞ አይጠፋም…not in a bad way of course, but FOMO (Fear Of Missing Out) can be a tempting mistress: from dinner parties, to coffee dates, and the occasional chipping in for little ናታንs birthday parties.

Obviously, such unplanned occasions will disrupt your goals.

Indeed, saving requires discipline. Discipline will form smart habits and smart habits can build wealth in the long run.

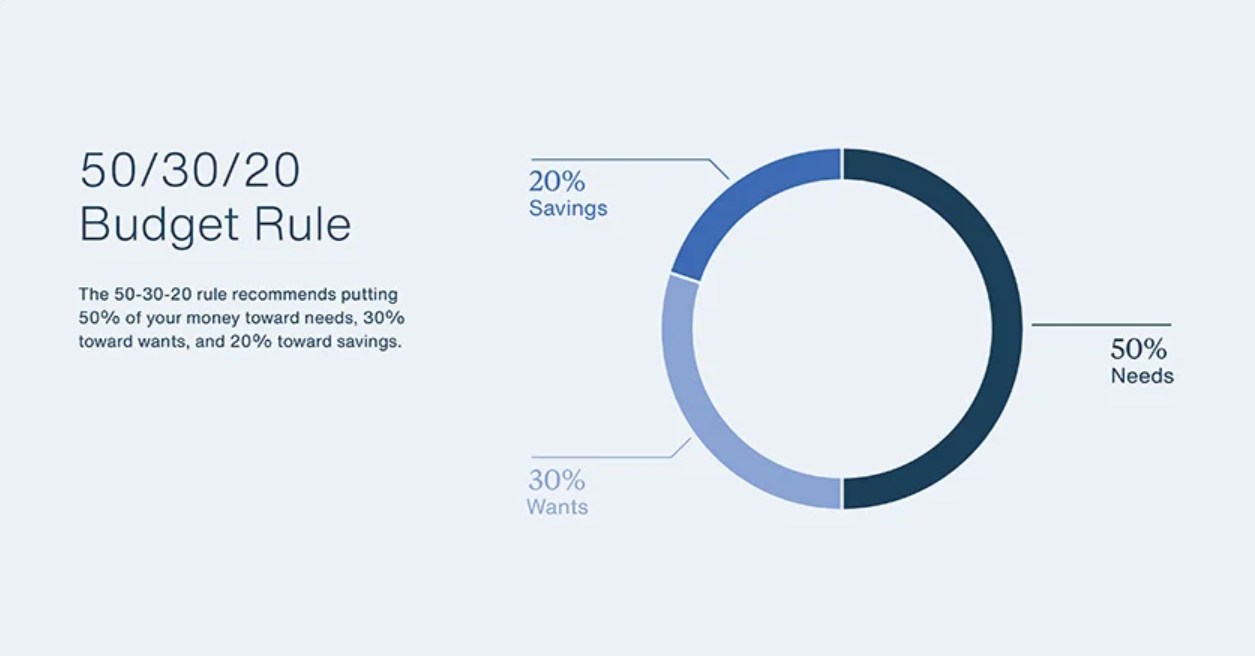

A common money management practice is the ‘50-30-20 rule’, whereby:

You spend 50% of your income on essentials (Rent, housing costs, groceries, gas etc.)

30% on non essentials like clothing, eating out, gym membership etc.

And 20% goes to your savings accounts, pension, investments etc.

Source: unfcu.org

Now is this a cardinal rule? Not at all.

But it does give a structure, a framework so to speak, on which to expand on.

One way to maximize this behavior is to involve friends and family, encourage everyone within the group to take common accountability and stick to the rule.

Gamify it if possible too where individual and group milestones are celebrated with a ‘cheat day’ like a trip to (K)KFC🍗!

Full disclosure: We’re unsure if a cheat day at ‘Kinda-KFC’ is a treat or a threat.

Key Takeaways

Cheque It Out: Cheques may be a classic payment tool, but they’re not foolproof—fraud and legal risks are real. For a more secure option, opt for a Cashier’s Payment Order (CPO) to guarantee timely payments with less drama.

Cash Rules: Money comes and goes but how we disperse it can lead to unwanted consequences. The 50/30/20 is a well know money management concept that can be applied if you’re having trouble finding some structure. Get close ones involved too to maximize its effectiveness.

Thanks for sticking with us, ፍራንክ family! Keep those wallets smart and your inbox open - we’ll be sliding in next week!

Reply